Thread:

Thread:

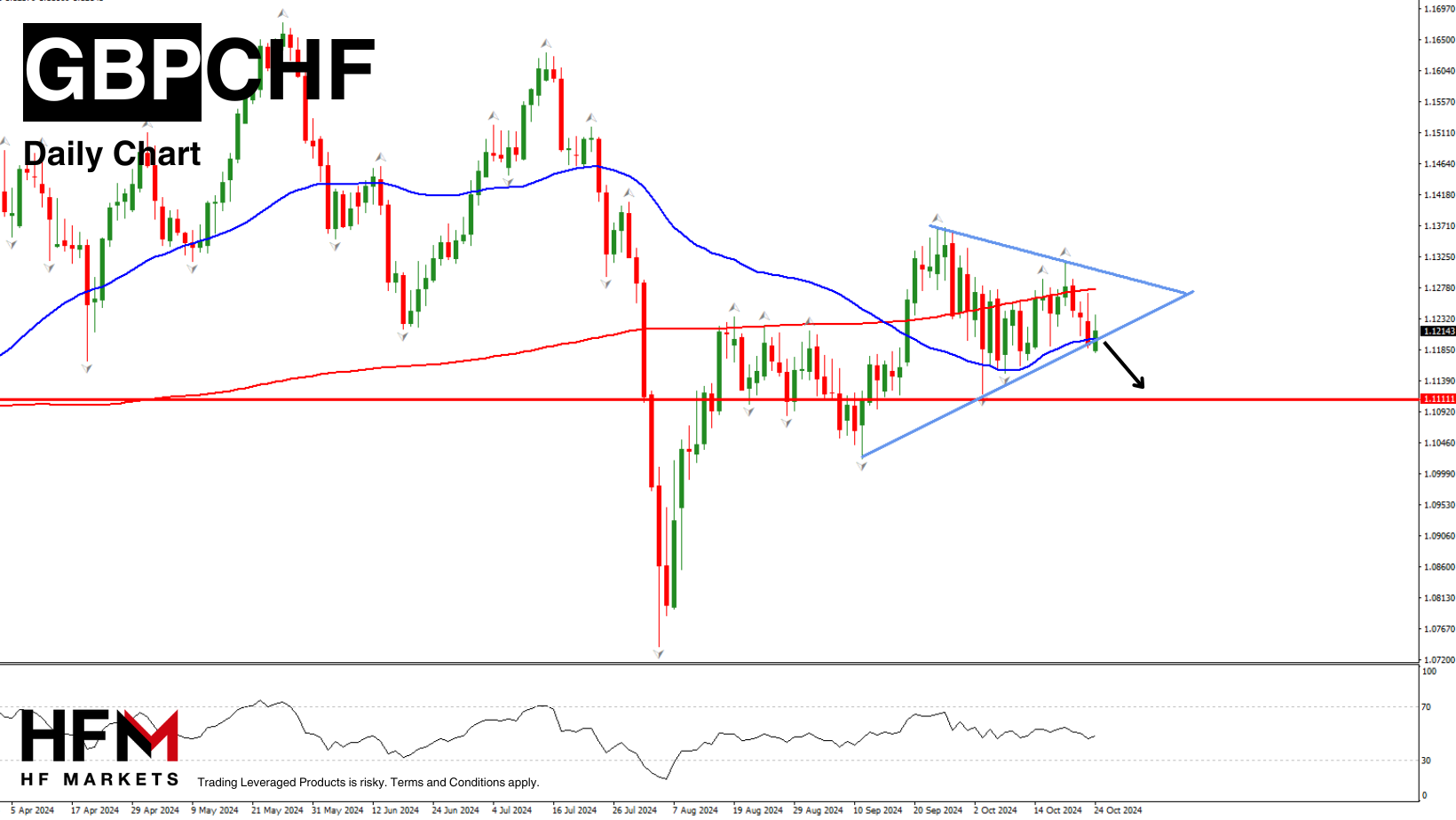

Date: 24th October 2024.

Mixed earnings, Stocks rebound, Dollar in a pull back.

Trading Leveraged Products is risky

Asia & European Sessions:

*Treasuries extend losses on anxieties and uncertainties, rise in yields hits stocks. Election jitters remain prominent, along with geopolitical worries.

*Wall Street was hammered also as some earnings disappointed, and bad news from some tech companies. An E. coli outbreak at McDonald’s also impacted.

*Expectations for deficit financing no matter who wins the election, and the concomitant surge in debt are further exacerbating inflation fears. A tepid 20-year auction added to the market’s woes.

*Fed’s Beige Book showed moderate growth and prices, decent labor market. US existing home sales fell -1.0% to 3.840 mln rate.

*Bank of Canada cut its overnight target rate by -50 bps to 3.75%, as widely expected. This is a 4th straight cut and ties the lowest rate since October 2022. While the statement indicated the timing and pace of future action will be guided by data, it was also indicated that more cuts are likely if the economy evolves as expected. The jumbo-sized cut is meant to boost growth and keep CPI close to 2%.

*Eurozone Composite PMI lifted to 2-month high of 49.7 in October from 49.6 in the previous month. German data actually came in somewhat better than expected, while French reports disappointed. The marginal improvement in the headline still leaves the Composite PMI in contraction territory, with new orders falling for a fifth consecutive month and at a similar pace as in September.

*UK October flash services PMI 51.8 vs 52.4 expected.

Financial Markets Performance:

*The NASDAQ lost -1.60%, with the S&P500 tumbling -0.92%, while the Dow slid -0.96%.

*The USDIndex hit 104.40, breaking the April-June support which turned into a key Resistance level. It rallied against all G10 peers.

*The USDJPY closed at 152.70 after paring its jump to 153.185, the highest since July amid risk the LDP and coalition partner Komeito could lose their majority at the weekend general election.

*The USDCAD settled back to 1.3825 after the BoC’s jumbo -50 bp cut and dovish guidance.

*Oil prices increased 1.9% to $70.54 per barrel.

*Gold fell -1.19% to $2716.17 per ounce after several fresh record highs.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work.

Andria Pichidi

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Bitcoin Forex Forum

Forex Community Place

Reply With Quote

Reply With Quote